If your credit score is sitting around 600, you are not alone. Millions of people fall into this “fair” range. The good news? You are closer to 700 than you think.

When you improve your credit score from 600 to 700, you unlock better loan approvals, lower interest rates, higher credit limits, and stronger financial opportunities. Even a 50–100 point increase can save thousands of dollars over time.

In this step-by-step guide, I will walk you through proven credit score improvement strategies that work in real life—not theory. These are the same tactics credit repair professionals use to help clients move into the “good credit” range.

Let’s get started.

What a 600 Credit Score Really Means

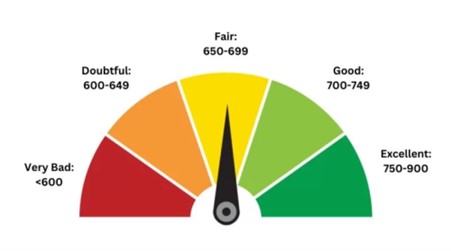

A 600 credit score is considered “fair” under most FICO and VantageScore models. Lenders see it as a moderate risk. You may qualify for credit cards and loans, but you will likely pay higher interest rates.

This range often results from:

- Late payments

- High credit card balances

- Limited credit history

- Collections or charge-offs

The important part? A 600 score is recoverable.

Why Reaching 700 Changes Everything

Moving from 600 to 700 shifts you from “fair” to “good” credit.

That means:

- Better mortgage rates

- Lower auto loan interest

- Higher credit limits

- Easier apartment approvals

- More premium credit card offers

Even a 1–2% interest difference on a mortgage can mean tens of thousands saved over time.

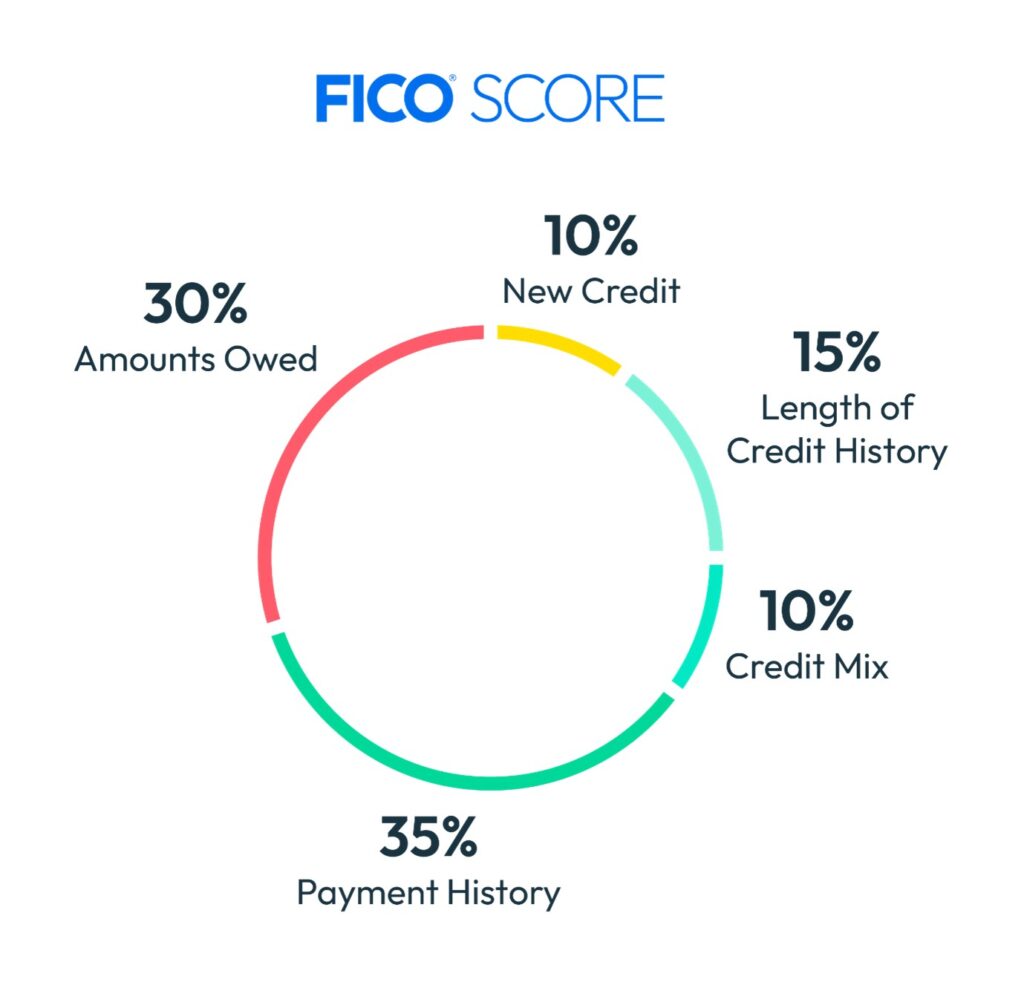

How Credit Scores Are Calculated

To improve your credit score, you need to understand what impacts it.

Here’s how FICO typically breaks it down:

- Payment History (35%)

- Credit Utilization (30%)

- Length of Credit History (15%)

- Credit Mix (10%)

- New Credit Inquiries (10%)

If your score is 600, usually the biggest issues are payment history and utilization.

Step-by-Step: How to Improve Your Credit Score from 600 to 700

Now let us break this down into practical action steps.

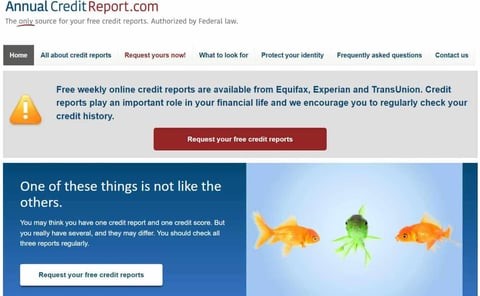

Step 1: Pull Your Credit Reports (Free)

Before anything else, check your reports from:

- Experian

- Equifax

- TransUnion

Use AnnualCreditReport.com (official U.S. site) to review all three.

Look for:

- Late payments

- Collections

- Errors

- High balances

- Duplicate accounts

You can’t fix what you don’t see.

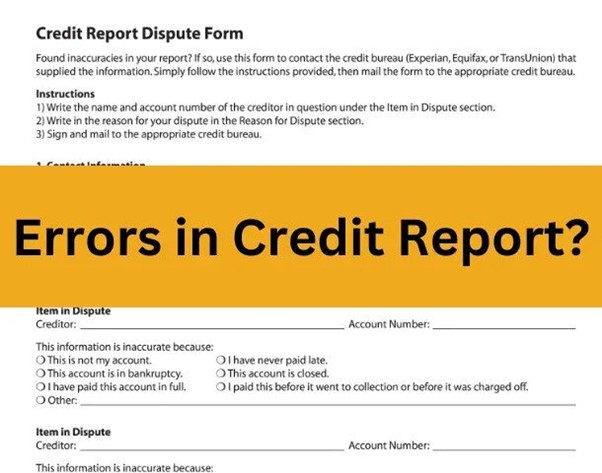

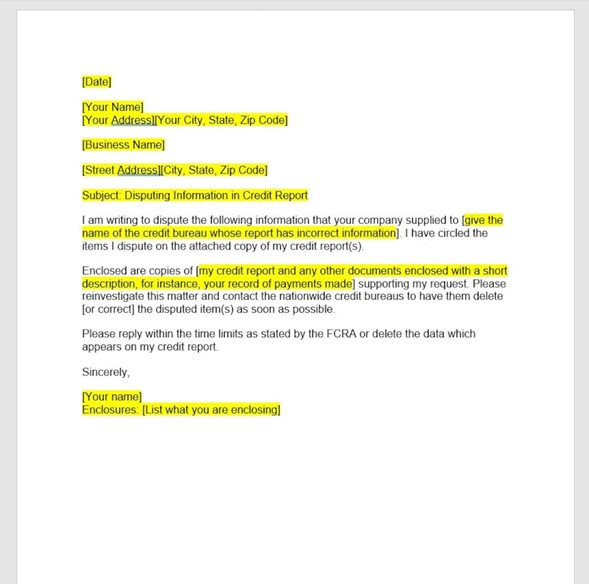

Step 2: Dispute Errors Immediately

Errors are more common than people realize. These might include:

- Accounts that aren’t yours

- Incorrect late payment dates

- Paid debts marked unpaid

- Duplicate listings

File disputes directly with the credit bureau online.

If an item is inaccurate and gets removed, your score can increase quickly—sometimes within 30 days.

This is one of the fastest credit score improvement strategies available.

Step 3: Lower Your Credit Utilization (Fast Impact)

Credit utilization is the percentage of available credit you are using.

Definition (Featured Snippet Optimized):

Credit utilization is the ratio between your credit card balances and your total credit limits. It makes up about 30% of your credit score. Keeping utilization below 30%—and ideally under 10%—can significantly improve your credit score.

Example:

- Credit limit: $5,000

- Balance: $4,000

- Utilization: 80% (too high)

To improve:

- Pay down balances aggressively

- Request credit limit increases

- Spread balances across cards

Pro tip: Pay your balance before the statement closing date—not just before the due date.

Step 4: Fix Late Payments (The Right Way)

Payment history has the biggest impact.

If you have:

- Recent late payments (under 24 months)

- One or two isolated 30-day lates

You can try a goodwill letter. Politely ask the lender to remove the late mark, especially if you have been consistent since.

For serious delinquencies:

- Bring accounts current ASAP

- Set up automatic payments

- Never miss another due date

One year of perfect payment history can significantly improve your credit score.

Step 5: Handle Collections Strategically

If you have collections:

- Verify the debt first.

- Request written validation.

- Negotiate a “pay for delete” if possible.

- Get agreements in writing before paying.

Not all paid collections increase your score immediately, but removing them can help.

Step 6: Add Positive Credit (If Needed)

If your file is thin, consider:

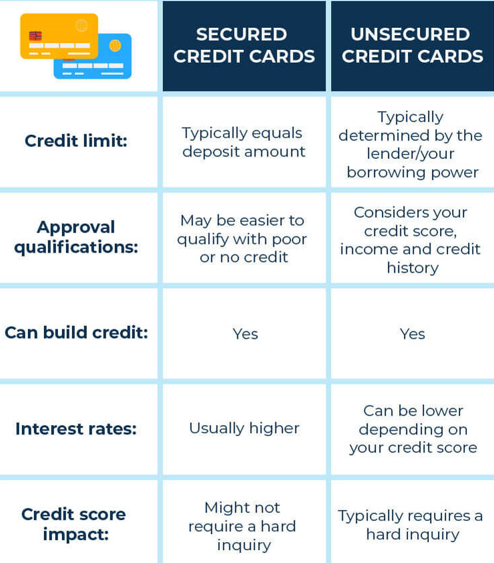

- Secured credit cards

- Credit builder loans

- Becoming an authorized user

Being added to a well-managed, low-balance credit card (with perfect payment history) can give your score a boost.

Step 7: Avoid New Hard Inquiries

While rebuilding:

- Don’t apply for multiple credit cards

- Avoid unnecessary financing

- Space out applications

Too many hard inquiries lower your score temporarily.

30-60-90 Day Credit Improvement Plan

Here’s a practical roadmap.

First 30 Days

- Pull reports

- Dispute errors

- Pay down high balances

- Set up auto-pay

Days 30–60

- Negotiate collections

- Request goodwill adjustments

- Ask for credit limit increases

Days 60–90

- Maintain under 30% utilization

- Keep all payments on time

- Avoid new credit applications

Many people see measurable score movement within 60–90 days.

Credit Score Comparison Table

| Credit Score | Rating | Loan Approval Odds | Interest Rates |

| 580–669 | Fair | Moderate | High |

| 670–739 | Good | Strong | Lower |

| 740–799 | Very Good | Very Strong | Very Low |

| 800+ | Excellent | Exceptional | Best Available |

Moving from 600 to 700 dramatically changes lender perception.

Common Mistakes That Keep You Stuck

Avoid these:

- Paying only minimum balances

- Closing old credit cards

- Ignoring small collections

- Applying for too much credit

- Missing due dates by a few days

Even one new 30-day late payment can undo months of progress.

Advanced Credit Score Improvement Strategies

If you want faster progress:

1. AZEO Method (All Zero Except One)

Keep all cards at zero except one reporting under 10%.

2. Rapid Rescore (Mortgage Situations)

If applying for a mortgage, lenders can sometimes update your report quickly after balance paydowns.

3. Strategic Balance Timing

Lower balances before statement closing dates to optimize reported utilization.

These techniques are often used by credit professionals to help clients cross into the 700 range.

Key Takeaways

- Payment history and utilization matter most.

- Keep balances under 30% (under 10% is ideal).

- Dispute inaccuracies immediately.

- Never miss a payment again.

- Consistency over 3–6 months produces real change.

Conclusion: Your 700 Score Is Closer Than You Think

Improving your credit score from 600 to 700 isn’t about luck. It’s about strategy and consistency.

Focus on:

- Perfect payment history

- Low credit utilization

- Cleaning up errors

- Adding positive accounts carefully

Small, disciplined actions repeated monthly create powerful results.

Start today. Pull your credit report. Make one extra payment. Set up autopay.

Your future approvals—and your wallet—will thank you.

Frequently Asked Questions (FAQs)

1. How long does it take to improve your credit score from 600 to 700?

Most people can achieve this in 3 to 6 months with consistent payments and lower utilization. Severe delinquencies may take longer.

2. Can I raise my credit score 100 points in 30 days?

It’s possible but rare. Rapid increases usually happen when errors are removed or high balances are paid off.

3. Does paying off collections improve credit score?

Sometimes. Newer scoring models ignore paid collections, but removing them entirely has stronger impact.

4. Should I close credit cards to improve my score?

No. Closing cards can increase utilization and shorten credit history.

5. What is the fastest way to improve credit score?

Lowering credit utilization and disputing errors are typically the fastest methods.